Private Equity Secondary Market – General

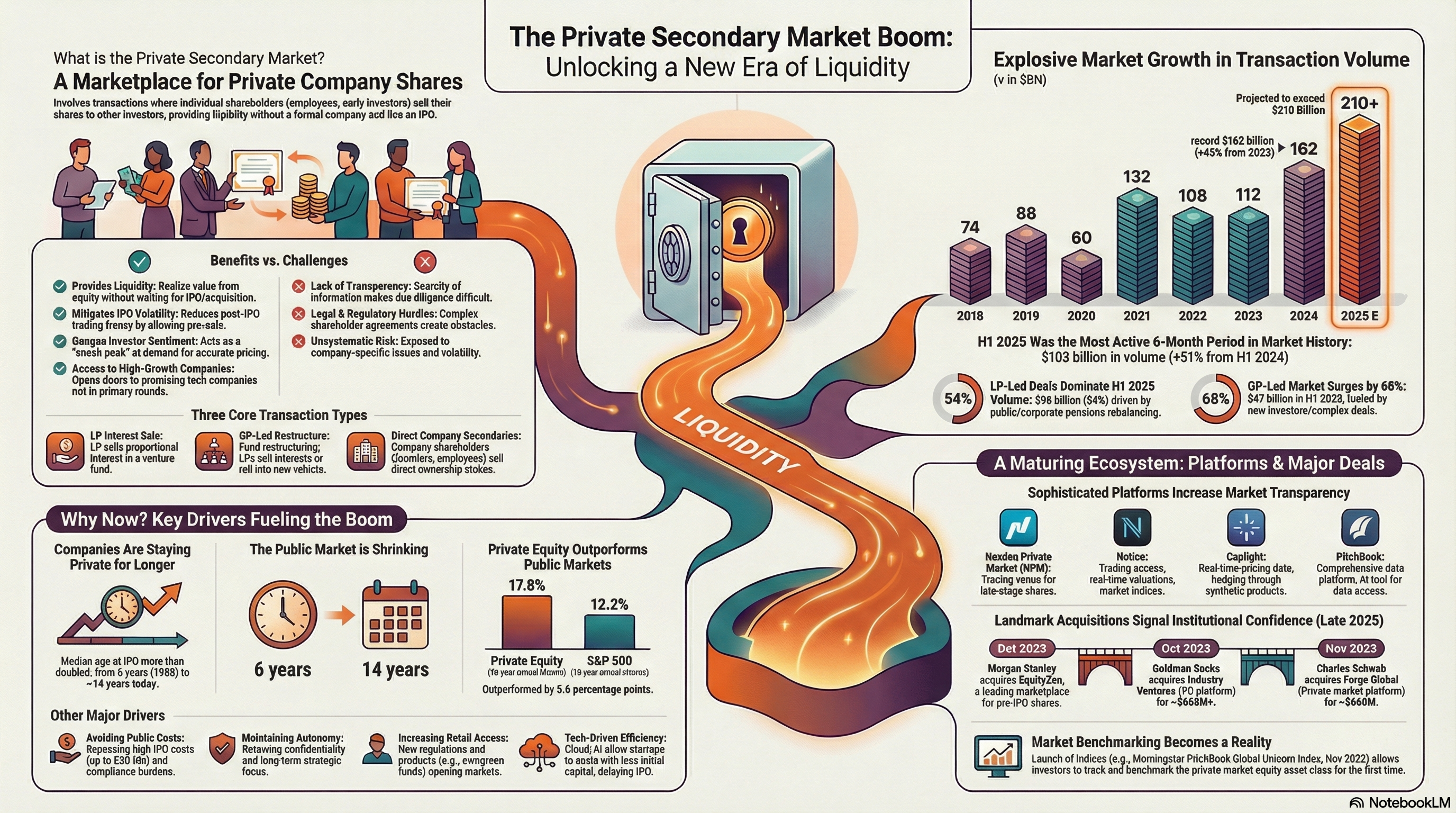

According to Pitchbook (What are direct secondary markets, Pitchbook, June 12, 2019), direct secondary markets involve transactions between individual shareholders (like general partners or employees) who sell/buy shares in a venture-backed company instead of selling/buying shares from the company itself.

One of the main populations to utilize the direct secondary market are the employees of privately held companies who receive equity compensation. GPs and founders also commonly participate in direct secondary markets as they often have equity in portfolio companies.

Due to the illiquid nature of private company shares, direct secondary markets serve as a mechanism to provide liquidity for those who own individual private company shares. These transactions give investors the opportunity to realize value and return capital without a full exit. For employees who own equity in a company, it can take years until they are able to realize the value of their shares. Lengthening exit times further exacerbate this challenge as it is taking increasingly longer to receive liquidity this way.

Secondary transactions can also help mitigate potential volatility when a company is first publicly listed. Shareholders who need liquidity get the opportunity to sell beforehand, which limits an early trading frenzy. Plus, a secondary sale can help gauge investor sentiment, essentially providing a sneak peek at the demand for a company’s shares and determining a more accurate price. Direct secondaries also allow investors to gain access to high-growth and emerging technology companies that they were not able to access in the primary markets.

One of the greatest challenges is the general lack of transparency and scarcity of information on opportunities in the direct secondary markets. This opacity can make it difficult to efficiently conduct due diligence. Further, this market poses legal and regulatory obstacles due to the complexity of shareholder agreements and their impact on secondary transactions.

Overall, each individual company’s shares have their own unique characteristics and challenges that investors must consider. Like purchasing just one stock, there is a lot of unsystematic risk involved in a direct secondary market transaction, depending on company-specific issues. Some investors have concerns regarding the potential for volatility due to limited supply and a generally illiquid market.

Venture Capital secondaries transactions can be split into two main categories: direct interest transactions and fund interest transactions. Each has unique attributes, dependent on the parties involved, resulting in a market of three core secondary transaction types:

- LP Interest – a Limited Partner (“LP”) in a venture fund chooses to sell its pro-rata interest to a buyer

- GP Led Restructure – a structured process where LPs are given the opportunity to seek liquidity through a fund restructuring. LPs may either choose to sell interests or to roll interests into new fund vehicles with reset economics.

- Direct Company Secondaries – Company shareholders, early-stage investors or long-term employees sell ownership interests. These can be in the form of individual transactions or structured tender processes orchestrated by Companies or brokers.

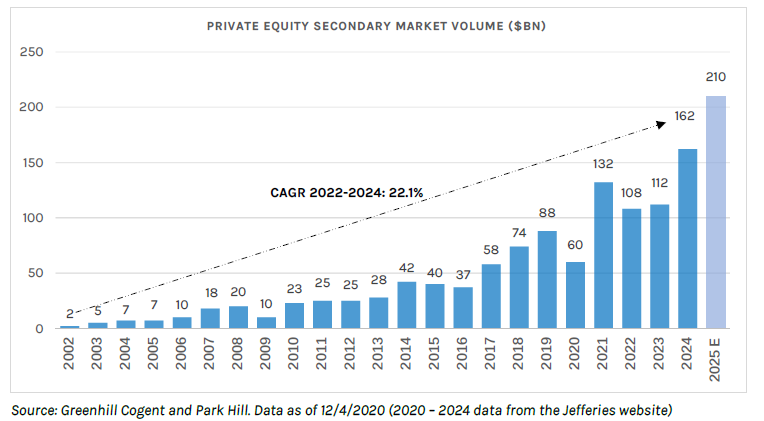

As is shown further (see further the “PE Secondary Market Deal Volume” Chart), the private capital secondaries market is growing, with 2021 and 2024 as record years. While the global pandemic has certainly worsened liquidity concerns for some investors, these sellers exist in all market conditions, as liquidity issues are not necessarily correlated to macro conditions, particularly among high-net worth individuals and smaller family offices.

Historically, the secondary market within private markets has lent itself to the buyout universe and has traditionally been perceived as a market for investors to sell their holdings under distressed circumstances at a significant discount. However, over the past decade a significant emergence of the VC secondary market occurred. The changes have presented a vastly different opportunity set for both sellers and buyers looking to secondary sales as a portfolio management tool to either obtain liquidity where sufficient returns have been realized or to seek “hard to access” investment opportunities in high growth VC backed companies. There are several distinct dynamics that differentiate the buyout market from the VC secondary market, driven by several key factors, including:

- Due Diligence & Sourcing – Venture is a difficult asset class to diligence due to the lack of information at the company level, therefore the need to have deep relationships to identify price and source opportunities is critical. This inefficiency is the source of the higher returns available in the VC market vs the buyout market.

- Fewer Brokers Involved – Venture secondaries are smaller in Net Asset Value (NAV) and overall transaction size relative to buyout counterparts. Since brokers get paid on commission, they tend to gravitate towards the higher dollar transactions, leaving fewer intermediaries that focus on the venture asset class.

- GP Transfer Restrictions – GPs, especially top quartile performing GPs, are highly restrictive regarding who you can transfer or sell an interest to. When this happens, the buyer universe becomes quite limited, often consisting only of existing LPs.

- Limited Buyer Universe – The buyer set in venture is severely limited relative to the buyout secondary market and other alternative asset classes. This has subsequently allowed for less competition within the VC market.

- Macro Environment – the added uncertainty and volatility that COVID-19 has brought to the market has resulted in a clear distinction between the thriving companies within traditional venture-backed sectors such as software, tech enabled businesses services companies and healthcare, while the traditional PE buyout companies have experienced their own challenges resulting in discounts and subsequent arbitrage value-add. As a result, the VC secondary market has typically thrived during times of uncertainty.

- The VC secondary market continues to demonstrate a win/win dynamic for all key stakeholders involved in a direct or fund secondary sale.

- LP and Shareholder Benefits (Sellers) – the VC secondary market has emerged as a viable exit and liquidity path for funds and shareholders including founders, early employees, or seed investors. While sellers still could lock in gains from high performing investments, they do not need to wait for an IPO or sale to achieve full liquidity and instead can consider liquidity options for partial or full liquidity through a secondary transaction.

- GP Benefits (Sellers) – GPs have an array of options to strive to achieve liquidity, generate cash on realized gains, while receiving monetized carry and resetting economics on a new fund vehicle. GPs are incentivized to pursue these deals as 1) they may be able to achieve previously unrealized value in their portfolios and 2) they are able to continue to steward their portfolios going forward with additional economics. Additionally, and as a result the relationship driven industry, the higher caliber GPs are afforded the opportunity to hand-select which LPs they want to purchase direct or fund interests.

- Investors (Buyers) – The infamous J-Curve is a great illustration of where investors with a secondary portfolio can leverage an opportunity to invest in a unique risk reward portfolio with often discounted assets that possess meaningful upside and shorter-term liquidity horizons. However, the scarcity of information and the need to have deep relationships to access deals and perform the right level of due diligence will remain critical to succeeding in the secondary VC market.

Secondary Market – Transaction Volumes

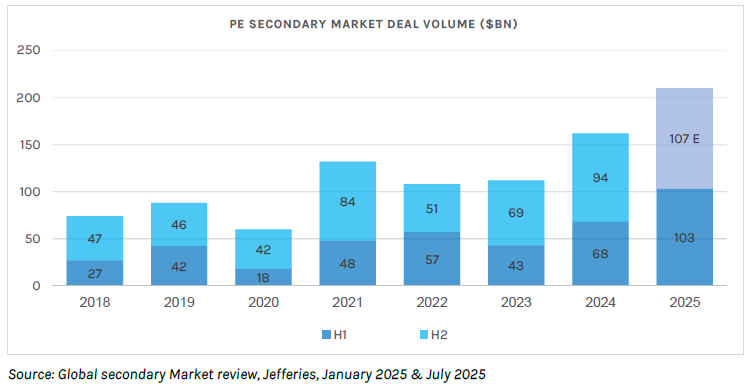

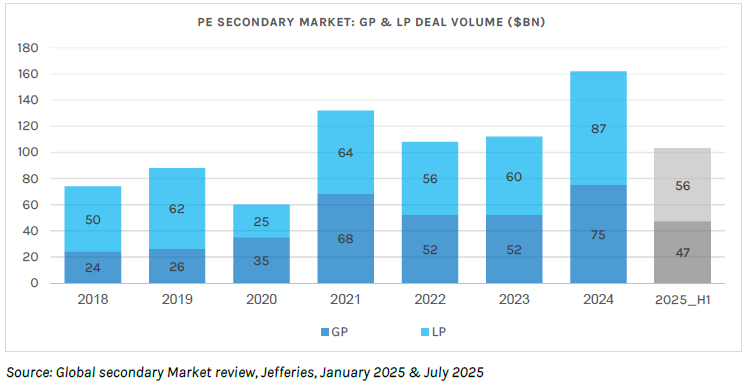

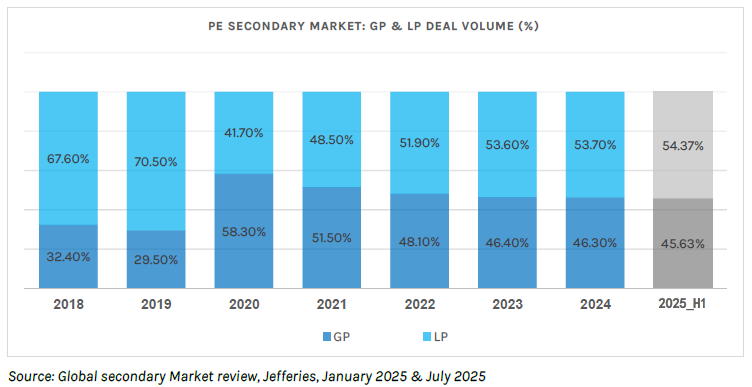

According to Jefferies (Global secondary Market review, Jefferies, January 2025), Global secondary volume reached $162 billion in 2024, representing a 45% increase from 2023 volume of $112 billion. The market gained momentum throughout the year with H2 volume of $94 billion (relative to $68 billion in H1), buoyed by a strong desire from LPs and GPs to accelerate liquidity along with increasing public markets helping to boost investor confidence.

In contrast to the prior volume record of $132 billion in 2021, which was driven in part by the transaction lull in 2020 due to COVID-19, the tailwinds that propelled 2024 activity to new heights appeared poised to stay, and even strengthen, in 2025.

In the first half of 2025, the secondary market set a record with $103 billion of volume, eclipsing the prior record of $68 billion in H1 2024. This represents a 51% increase from H1 2024, and it is the largest year-over-year H1 volume increase and the most active 6-month period in market history. This unprecedented growth puts the market at pace to exceed $210 billion in total volume by year-end. This expansion reflects continued momentum across both LP and GP-led segments, underpinned by a combination of robust supply and sustained demand.

Market volume was driven by multiple tailwinds, including the lack of distributions from standard IPO and M&A pipelines fueling supply and diversified expanding pools of secondary capital fueling demand (H1 2025 Global Secondary Market Review. Jefferies, July 2025).

The LP-led market experienced $56 billion of transaction volume in H1 2025 (54% of total transaction volume), which represents a 40% increase to H1 2024 volume. The surge in activity was driven by broad-based selling across all LP types, creating a variety of supply across deal size, portfolio quality and underlying asset strategy. The bulk of activity (48% of total LP volume) was from public and corporate pensions, as many are overallocated to private equity and used the secondary market to manage liquidity and rebalance their portfolios. The potential increase in endowment excise tax by 2026 was largely publicized and indirectly led to increased selling to accelerate realization of gains, as endowments and foundations accounted for 16% of total LP volume (up from 7% in H1 2024).

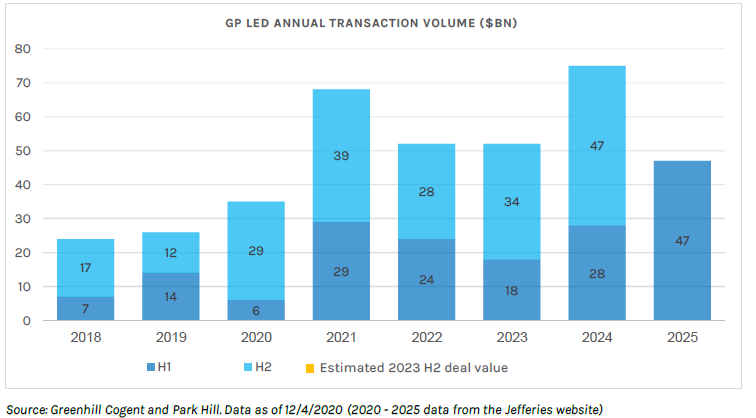

GP-led secondary volume reached $47 billion in H1 2025, marking a 68% increase over the same period in 2024. This surge reflects the growing maturity and diversification of the GP-led market, driven in large part by the entrance of new investor groups that have reshaped market dynamics. These entrants, ranging from institutional investors to specialized secondaries funds, have brought fresh capital and a greater appetite for complex, bespoke transactions. As a result, certain asset classes have seen notable growth, particularly credit, venture and real asset continuation vehicles. These strategies, which investors once considered niche, have gained broader acceptance as GPs seek to extend ownership of high-performing assets while providing liquidity options to existing LPs.

Secondary Market – Outlook

According to Jefferies (H1 2025 Global Secondary Market Review. Jefferies, July 2025 , the secondary market is well-positioned for continued growth and innovation in H2 2025, building on the record-setting first half. With an expanding buyer universe, increasing adoption of creative liquidity solutions and competitive pricing levels, it is expected that both LP and GP-led markets will continue to thrive.

Jefferie’s expectations are that evergreen retail capital and traditional secondary market fundraising will continue to expand, providing ample liquidity to support diverse transactions. LP and GP-led markets will maintain an approximately even volume split with an even greater number of $1 billion or larger deals. These dynamics, combined with a positive macroeconomic outlook and continued expansion of overall private capital strategies, set the stage for 2025 to be a landmark year in the secondary market.

Private Equity Markets

(Based on BofA research “Unicorns, Decacorns and Hectocorns: The Private Companies Primer”, Oct 2025)

The rise of private markets

According to EY and McKinsey, total assets under management (AUM) in private markets have expanded substantially, increasing from roughly $9.7 trillion in 2012 to approximately $22 trillion by 2024. McKinsey data further indicates that between 2000 and 2023, private-market AUM multiplied nearly twentyfold. Looking ahead, Boston Consulting Group projects continued momentum, with expected 2023–2028 compound annual growth rates of at least 11% across private equity, private credit, and infrastructure strategies.

In the United States, private markets have outpaced the growth of public markets significantly, expanding around 35 times over the past 25 years, compared with a fourfold increase in public-market size. Consequently, private markets’ share of total U.S. market AUM is estimated to rise from 1% in 2000 to 8% by 2025.

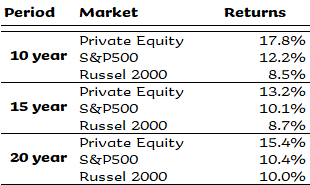

While public companies might seem more conducive to effective capital allocation due to their transparency, governance standards, and liquidity, investors have increasingly shifted toward private-market strategies. The key driver is performance: over a ten-year period, private equity delivered superior returns, outperforming the S&P 500 by 5.6 percentage points annually and the Russell 2000 Growth Index by 9.3 percentage points. These results are presented in the following table:

Companies are staying private longer

Globally, the population of publicly listed firms has contracted by about 6% since 2019, now standing at roughly 3,000. In the United States, the shrinkage has been even more pronounced: the number of listed companies has nearly halved over the past quarter-century, declining from a high of 8,090 in 1996 to 6,917 in 2000 and then to approximately 4,010 by 2024. U.S. IPO volumes have also remained structurally lower than in the 1990s, averaging around 150 offerings per year since the introduction of Sarbanes-Oxley in 2000, compared with roughly 500 annually during the prior decade. Companies are staying private longer as well—the median age at IPO has increased from six years in 1980 to about fourteen years today. Over the same period, the number of private businesses backed by private equity in the U.S. has expanded fivefold.

Drivers of the shift toward remaining private

Higher public-company costs and compliance requirements

One major factor motivating firms to stay private is the desire to avoid the higher expenses, regulatory burdens, and disclosure requirements associated with public-company status. For instance, a private business generating revenues and pursuing a transaction in the $100–249 million range faces average IPO-related costs of roughly $6.9–30.5 million. Underwriting fees represent the largest share of these expenses, typically amounting to about 4–7% of gross IPO proceeds.

Public companies must also adhere to extensive regulatory frameworks, including Sarbanes-Oxley (SOX), which mandates strict standards for revenue recognition, auditing, internal controls, and record retention, as well as more robust documentation and reporting infrastructure. These obligations translate into substantial ongoing costs: for the median U.S. listed firm, total compliance expenditures equate to approximately 4.1% of market capitalization.

Privacy, autonomy, and control drivers

By design, private companies operate with significantly more confidentiality, as they are not obligated to release detailed financial information, strategic plans, or intellectual property to the public or to competitors. This allows them to retain tighter control over sensitive aspects of the business. In addition, they are insulated from the short-term performance expectations often imposed by public shareholders who prioritize quarterly results. As a result, private firms have greater flexibility to pursue long-range strategic priorities, including substantial capital projects, R&D, and innovation initiatives, even when these choices may reduce near-term earnings.

The increasing need for scale

The average market capitalization of a U.S. publicly traded company rose to about $15.5 billion in 2024, compared with roughly $0.3 billion in 1975, an increase of nearly 60 times. Over the same period, the total value of the U.S. listed equity market expanded by approximately 88 times. Today, the combined market capitalization of U.S. equities is roughly twice the size of U.S. GDP, a reflection of both sustained market appreciation and the growing scale of public companies.

While this expansion enhances the global competitiveness of publicly listed firms, it simultaneously creates a more challenging environment for private companies planning to go public, as they face a landscape dominated by significantly larger incumbents.

Accelerated decisions that drive tech advancements

Technological breakthroughs, such as cloud computing, AI agents, and generative AI, are reducing both upfront investment requirements and ongoing operating expenses for many technology-driven businesses. As a result, companies can scale and achieve substantial valuations with far less initial capital, allowing them to stay private longer and delay entering the public markets. Within private firms, decision-making tends to be more streamlined, unencumbered by large boards, multiple committees, or frequent shareholder approvals. Empirical evidence also shows that a 1% increase in private equity investment is associated with a 0.04–0.05% rise in patents granted by the U.S. Patent and Trademark Office (USPTO).

Rising access to private markets

Private markets have historically been limited to institutional investors, family offices, and ultra-high-net-worth individuals, placing them largely beyond the reach of typical retail investors. Significant minimum capital requirements and limited liquidity made private assets unsuitable for most retail portfolios. However, recent industry shifts, such as product innovation and evolving regulatory frameworks, are beginning to expand retail access and may drive meaningful growth in future retail alternatives AUM.

For instance, in August 2025, the Trump administration issued a directive instructing regulators to broaden the availability of alternative investments within 401(k) plans. Similarly, in March 2025, the Monetary Authority of Singapore (MAS) proposed the Long-Term Investment Fund (LIF) framework, designed to give retail investors access to private-market products. In the United Kingdom, 17 workplace pension providers have also committed to allocating 10% of their portfolios to alternative assets by 2030.

Innovation drives broader access to private markets

Investment vehicles in this space are often intricate, requiring substantial minimum commitments and imposing lengthy lock-up periods during which investors cannot redeem or sell their holdings. They also typically involve capital calls, formal requests for investors to provide portions of the capital they previously committed.

Nevertheless, several structures are helping broaden investor access to private markets. These include evergreen funds (open-ended vehicles without a predetermined end date or lock-up period and typically featuring lower minimum investments), sidecars (arrangements in which one investor permits another to direct how the committed capital is deployed), feeder funds (vehicles that pool investor commitments into a master fund that manages all underlying investments), and funds of private funds (portfolios that invest in multiple private funds). Many of these options are increasingly accessible to retail investors through wealth-management platforms.

Retail alternatives AUM projected to outpace alternatives industry growth

Retail assets represent a major growth opportunity for private markets over the coming decade. Bain forecasts that private wealth allocations to alternatives will expand to a 12% CAGR until 2032, compared with an estimated 8% CAGR for institutional capital, driven by investors’ desire for diversification, lower historical correlation to public markets, and stronger long-term return potential. (Based on BofA research “Unicorns, Decacorns and Hectocorns: The Private Companies Primer”, Oct 2025)

The broader implications

Corporate capacity for disruption

Since 1926, U.S. public markets have generated approximately US $55 trillion in shareholder wealth, yet only about 3% of listed companies were responsible for all of that net value creation. Although the dataset extends only through 2022, it is likely that the share of companies contributing to total net wealth creation has become even smaller in the period since.

The rising influence of disruptive companies is also reshaping the landscape for established incumbents. In U.S. public markets, for example, nearly one-third of the S&P 500 has turned over since 2015 (S&P Dow Jones Indices). The average tenure of a company in the index has declined sharply over time. in 1958, firms remained in the S&P 500 for an average of 61 years on a seven-year rolling basis. This fell to 30 years in the 1980s, dropped further to 24 years by 2016, and reached just 16 years by 2021.

Private companies, including unicorns, can be highly disruptive.

A unicorn refers to a privately held startup valued at $1 billion or more. Only about 0.07% of venture-backed software startups founded in the 2000s achieved this milestone, roughly one in every 1,538. Unicorn status stems from disruptive innovation, firms that fundamentally reshape their industries. This disruption may come from introducing a novel product, deploying new business models such as subscription services or gig-economy platforms, redefining customer expectations, or using technology to eliminate inefficiencies. Illustrative examples include Google, which transformed how people navigate the internet, Airbnb, which challenged the traditional hotel sector and Uber, which revolutionized urban transportation by addressing gaps in the taxi market.

Major impacts on listed firms and the broader economy

Understanding major developments within private companies is essential—not only for assessing how their products, positioning, and innovations influence publicly listed peers and industry ecosystems, but also for evaluating how their underlying technologies could reshape the global economy.

For example, ChatGPT, a large language model chatbot that was the first to bring generative AI to a mass audience, was developed by OpenAI, which now carries an estimated valuation of about $500 billion (Crunchbase, as of October 2025). Since its debut in November 2022, AI innovation has accelerated rapidly, from cutting-edge frontier models produced by firms such as Anthropic and xAI to advancements in physical AI, including humanoid robots, autonomous vehicles (e.g., Waymo), and defense-oriented drones (e.g., Anduril).

Private Market Data & Trading Platforms

In recent years, the private-market ecosystem, particularly the universe of late-stage startups and unicorns, has undergone significant transformations. The rapid maturation of secondary markets, the growing institutional demand for transparency, and the emergence of sophisticated data providers have collectively reshaped how investors access, analyze, and price private-company equity. These developments have accelerated the creation of platforms offering deeper market intelligence, real-time valuation insights, and increasingly efficient trading and liquidity solutions. Following is a short description of the existing main private markets data and trading platforms:

NPM – Nasdaq Private Market

- Provides a secondary trading venue for private company shares (mainly late‑stage / pre‑IPO).

- Supports company liquidity programs such as tender offers and employee liquidity events.

- Full digital workflow: onboarding, transaction matching, settlement, and market data tools.

- Progress in the last two years: launched the new generation of SecondMarket (2024), expanded electronic block‑trade capabilities, strengthened transparency and institutional infrastructure.

Notice

- Provides trading access to private/pre‑IPO equities through a network of brokers for retail and institutional investors.

- Offers real‑time valuations, market activity, funding round data, firmographics, and API-based data delivery.

- Portfolio monitoring tools, performance analytics, and market indices (e.g., Notice‑50).

- Progress in the last two years: expanded research and real‑time datasets, enhanced API capabilities, broadened indices universe, and strengthened retail + institutional trading infrastructure.

Caplight

- Provides real‑time private‑market pricing, trade insights, alerts, and valuation intelligence.

- Covers funding rounds, secondary transactions, mutual fund marks, and company performance metrics.

- Enables long/short exposure to private equities using synthetic and structured products, building a derivatives layer for the private market.

- Progress in the last two years: deeper data transparency, expanded company coverage, institutional partnerships, and growth of hedging/derivatives infrastructure.

PitchBook

- A comprehensive data platform for private capital markets: companies, funding rounds, investors, private equity, venture capital, private debt, M&A, and secondaries.

- Includes rich research reports, benchmarks, indices, and Excel-integrated data tools.

- Offers analytical tools for valuation, multiples, fund performance, fundraising, and market intelligence.

- Progress in the last two years: expanded datasets across all private‑market verticals, strengthened research layers, and launched PitchBook Navigator (2025), an AI tool enabling natural‑language access to private‑market data.

Development of tools for investment in the Private Equity market

Over the past few years, Morningstar and PitchBook introduced the first-ever widely accepted indices that attempt to track the market value of late-stage, venture-backed private companies, typically “Unicorns,” i.e. private companies with post-money valuations of at least USD billion. The flagship of these offerings is the Morningstar PitchBook Global Unicorn Index, launched in November 2022, which provides a global benchmark covering all eligible unicorns from Pitchbook’s database. The index employs a proprietary “mark-to-model” methodology, combining the company’s latest funding rounds, comparable private-market transactions, and public-market peers, to estimate daily valuations for companies that otherwise lack public market prices.

The emergence and gradual maturation of these indices mark a meaningful shift: private companies, long considered opaque and difficult to value, now have a set of transparent, repeatable, daily updated benchmarks. For the first time, investors can track the “private-market equity asset class” in a way roughly analogous to public markets, benchmark fund performance, perform asset allocation, and even build investable products (funds, ETFs, etc.) that reflect the late-stage-private segment.

Major Deals in the Secondary Market

Morgan Stanley Acquisition of EquityZen

On October 29, 2025, Morgan Stanley announced an agreement to acquire EquityZen, a leading platform for private company shares. This acquisition strengthens Morgan Stanley’s unique private-markets ecosystem, which offers private companies and their shareholders a comprehensive range of services—including cap-table management, tender and liquidity programs, direct and co-investment opportunities, and secondary trading.

EquityZen operates as a prominent marketplace for pre-IPO investment opportunities, facilitating transactions between shareholders of private companies and accredited investors. Leveraging advanced technology and data-driven tools, the platform provides insights that support its base of approximately 800,000 users in navigating private market dynamics. To date, EquityZen has executed over 49,000 private placements across nearly 500 private companies.

The integration of EquityZen into Morgan Stanley’s platform is positioned to meet evolving client requirements as companies remain private for longer periods. This includes the ability to offer structured, customizable liquidity solutions for employees and early investors through a streamlined and controlled process. By incorporating EquityZen’s private-shares marketplace alongside Morgan Stanley’s existing cap-table management capabilities, the combined offering is expected to deliver a more comprehensive, end-to-end solution for private-market companies.

Goldman Sachs’s acquisition of Industry Ventures

On October 13, 2025, The Goldman Sachs Group, Inc. (NYSE: GS) announced an agreement to acquire Industry Ventures, a prominent venture capital platform investing across all stages of the VC lifecycle. Goldman Sachs will acquire 100% of the equity of Industry Ventures.

The transaction consideration will consist of $665 million in cash and equity payable at closing and additional contingent consideration of up to $300 million, payable in both cash and equity, based on Industry Ventures’ future performance through 2030. The transaction is expected to close in the first quarter of 2026, subject to regulatory approval and conditions.

Founded in 2000, Industry Ventures oversees approximately $7 billion in assets under supervision and has executed more than 1,000 primary and secondary investments since its founding in 2000. According to the firm, its realized performance to date reflects a net IRR of 18% and a net realized MOIC of 2.2x across its platform. The firm is headquartered in San Francisco, with offices in Boston, Washington, DC, and London.

Industry Ventures has been an early mover in several areas of the venture capital landscape, including secondary liquidity solutions, seeding emerging venture capital managers, direct co-investments in early-stage high-growth companies through pro-rata rights, and investments at the intersection of venture capital and technology-focused buyouts. Industry Venture holds one of the largest U.S. portfolios of venture capital partnerships, spanning seed to late-stage growth, with exposure to more than 800 venture and technology-oriented funds. It collaborates with over 325 venture firms as a value-added limited partner, liquidity provider, and co-investment partner.

Following the acquisition, Industry Ventures will be integrated into Goldman Sachs’ External Investing Group (XIG), which manages more than $450 billion in assets under supervision across both traditional and alternative strategies. XIG is a major private-markets participant, active in co-investments, alternative manager strategies. The addition of Industry Ventures expands the platform’s technology-focused investment capabilities for Goldman Sachs’ global client base.

Goldman Sachs Asset Management has been a Limited Partner in Industry Ventures funds for over two decades and has offered strategies from Industry Ventures to its clients for a decade.

Charles Schwab Corporation acquisition of Forge Global Holdings, Inc.

The Charles Schwab Corporation (“Schwab”) announced on November 6, 2025, that it has entered into a definitive agreement to acquire Forge Global Holdings, Inc. (NYSE: FRGE) (“Forge”) in a transaction valued at approximately $660 million. Forge operates a leading private market platform and trading marketplace through which investors have collectively transacted more than $17 billion in private company shares.

Forge provides qualified investors with both direct and indirect avenues to access private-market opportunities. Its integrated offering includes a direct trading marketplace, private company solutions, and proprietary data. Forge aims to improve transparency and expand access for eligible investors. Forge is also preparing to launch interval funds designed to further broaden private market participation by offering lower costs and reduced investment minimums.

The acquisition advances Schwab’s strategy to expand private market capabilities for both retail investors and advisors, complementing its broader wealth, advisory, and investment management offerings to address increasingly complex client needs. Long term industry trends, coupled with growing investor interest in diversification, continue to support strong momentum in private markets. Private-wealth allocations to alternative asset classes are projected to increase from approximately $4 trillion today to an estimated $13 trillion by 2032.

Together, Schwab and Forge will unite private stock plan administration and liquidity access in a single, integrated ecosystem that benefits all participants. Through this acquisition, Schwab will build on Forge’s decade plus experience helping private companies deliver capital and liquidity solutions through a partnership model rooted in company approval and trusted collaboration.

Under the terms of the agreement, Schwab will acquire all of Forge’s issued and outstanding common shares for $45 cash per Common Share. The transaction is expected to close in the first half of 2026, subject to customary closing conditions, including approval by Forge’s stockholders and regulatory approvals. Forge’s two largest stockholders, Motive Capital and Deutsche Börse, have entered into agreements committing to support the transaction.

Register with The Elephant Today

Ready to unlock liquidity and learn how you can turn your equity into opportunity?